Malaysia’s Service Tax expansion in 2025 introduced significant changes for businesses, particularly those operating under long-term contracts such as rental, leasing, maintenance, and construction agreements.

One issue that quickly became a major concern was this:

“Will businesses lose the temporary Service Tax exemption if contracts were not stamped before 9 June 2025?”

The short answer: potentially yes, under the original policy conditions.

Understanding the Background

With the expansion of Service Tax effective 1 July 2025, many businesses were already tied to ongoing contracts signed before the implementation date.

To ease the transition, the Royal Malaysian Customs Department (RMCD) introduced a temporary relief mechanism for certain existing agreements known as “non-reviewable contracts.”

This relief was intended to prevent businesses from unfairly absorbing additional Service Tax costs where pricing had already been fixed contractually.

What is a Non-Reviewable Contract?

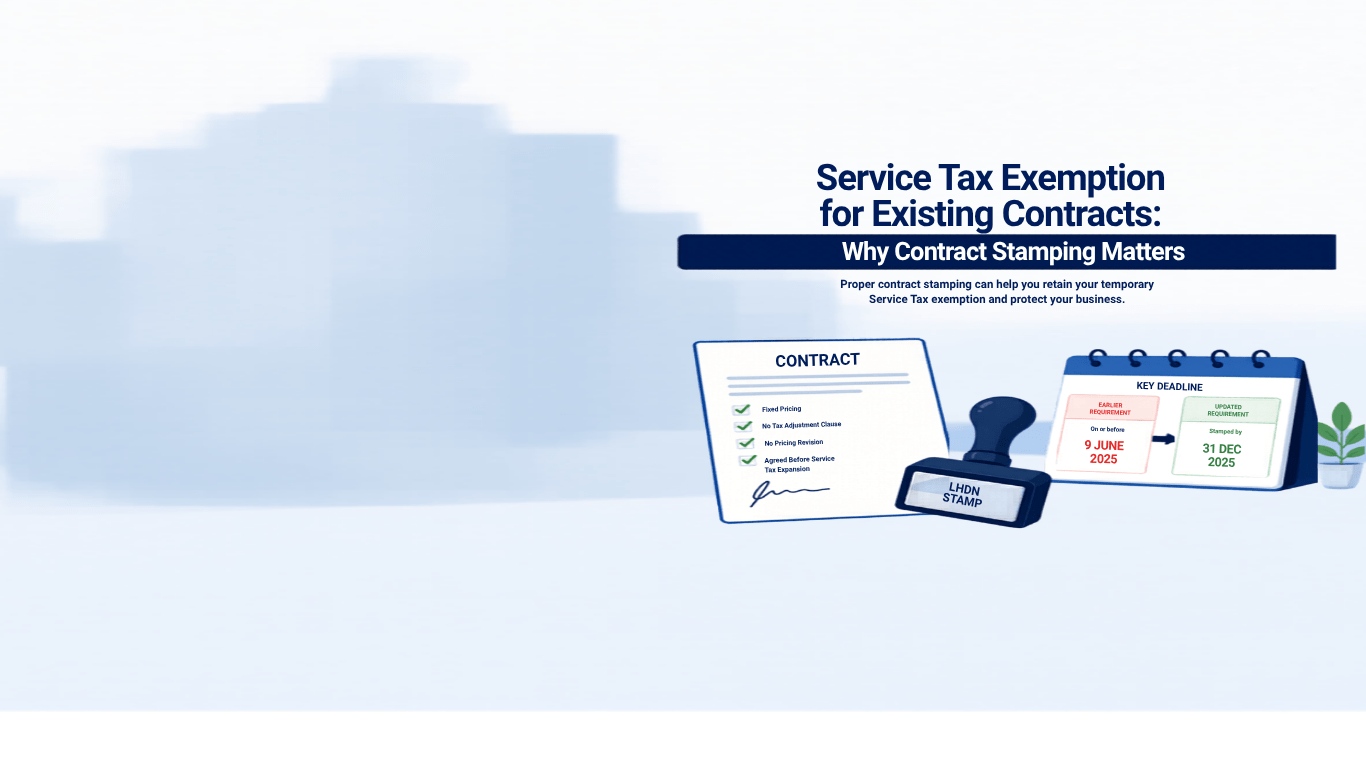

A non-reviewable contract generally refers to an agreement where:

- pricing is fixed,

- there is no tax adjustment clause,

- there is no pricing revision mechanism, and

- the contract terms were agreed before the Service Tax expansion.

In simple terms, businesses cannot revise pricing midway to recover the newly imposed Service Tax from customers.

Why the 9 June 2025 Deadline Became Critical

Under the earlier RMCD policy guidelines, one of the key conditions for exemption eligibility was that the contract must have been:

- signed, and

- stamped by LHDN

on or before 9 June 2025.

This created concern for many businesses because in practice, agreements are often signed first and stamped later.

As a result:

✅ Contracts signed and stamped before 9 June 2025 were generally eligible for temporary exemption.

❌ Contracts signed before the deadline but stamped afterwards risked failing the exemption condition.

This became especially significant for industries involving long-term contractual commitments such as:

- property rental and leasing,

- construction,

- maintenance services, and

- managed service arrangements.

Subsequent Relaxation by Authorities

Following industry feedback, the government later relaxed the stamping requirement through updated policy guidance.

The revised position generally allowed contracts signed before 1 July 2025 to qualify, provided stamping was completed by 31 December 2025.

This update provided much-needed relief to businesses that had genuine pre-existing contracts but had not finalized stamping procedures by the earlier deadline.

Key Takeaway for Businesses

Businesses should not treat contract stamping as merely an administrative formality.

For tax purposes, proper documentation and timely stamping can directly impact:

- exemption eligibility,

- Service Tax exposure,

- contractual cost recovery, and

- future audit defensibility.

Companies are encouraged to review existing agreements carefully to determine:

- whether contracts qualify as non-reviewable,

- whether stamping requirements have been fulfilled, and

- whether Service Tax implications have been properly assessed.

How We Can Help

Navigating SST transitional rules can be complex, particularly where contractual arrangements span multiple years or involve fixed pricing structures.

Our team can assist with:

- reviewing contract eligibility,

- assessing SST exposure,

- advising on transitional relief conditions, and

- supporting compliance documentation and risk management.

For further discussion, feel free to reach out to our team.

Leave a Reply